Rを利用して固定効果モデルによる回帰を考えます。

以下の資料を引用参照しています。

- https://de.meta-analysis.com/download/Intro_Models.pdf

- https://pmc.ncbi.nlm.nih.gov/articles/PMC8924903/

- https://www.fbc.keio.ac.jp/~tyabu/econometrics/econome1_8.pdf

- https://www.nishiyama.kier.kyoto-u.ac.jp/2020/jugyochukei4.pdf

- https://user.keio.ac.jp/~nagakura/zemi/panel.pdf

以下の固定効果モデルを考えます。 \[Y_{i\,t} = \alpha_{i} + \beta X_{i\,t} + \epsilon_{i\,t} \tag{1}\] ここで、 \(Y_{i\,t}\) : 個体 i の時点 t における従属変数、\(\alpha_i\) : 個体 i の固定効果(個体ごとの切片)、\(X_{i\,t}\) : 個体 i の時点 t における説明変数、\(\beta\) : 説明変数の係数(すべての個体で共通)、\(\epsilon_{i\,t}\) : 誤差項

始めに固定効果と説明変数との間に相関のあるサンプルデータを作成します。

seed <- 20250126

set.seed(seed = seed)

n_id <- 5 # 個体数

n_time <- 6 # 時間数

# データフレームの作成

df <- data.frame(

id = rep(1:n_id, each = n_time),

time = rep(1:n_time, times = n_id)

)

# 個体効果(固定効果)を生成

id_effects <- rnorm(n_id, mean = 2, sd = 0.5)

df$id_effect <- id_effects[df$id]

# 固定効果と相関のある説明変数xを生成

df$x <- df$id_effect + rnorm(n_id * n_time, mean = 0, sd = 1) # id_effectに依存

# 誤差項を生成

df$epsilon <- rnorm(n_id * n_time, mean = 0, sd = 1)

# 従属変数yを生成

beta <- c(2, 3.5)

df$y <- beta[1] + beta[2] * df$x + df$id_effect + df$epsilonサンプルデータを確認します。

library(dplyr)

library(ggplot2)

glimpse(df)

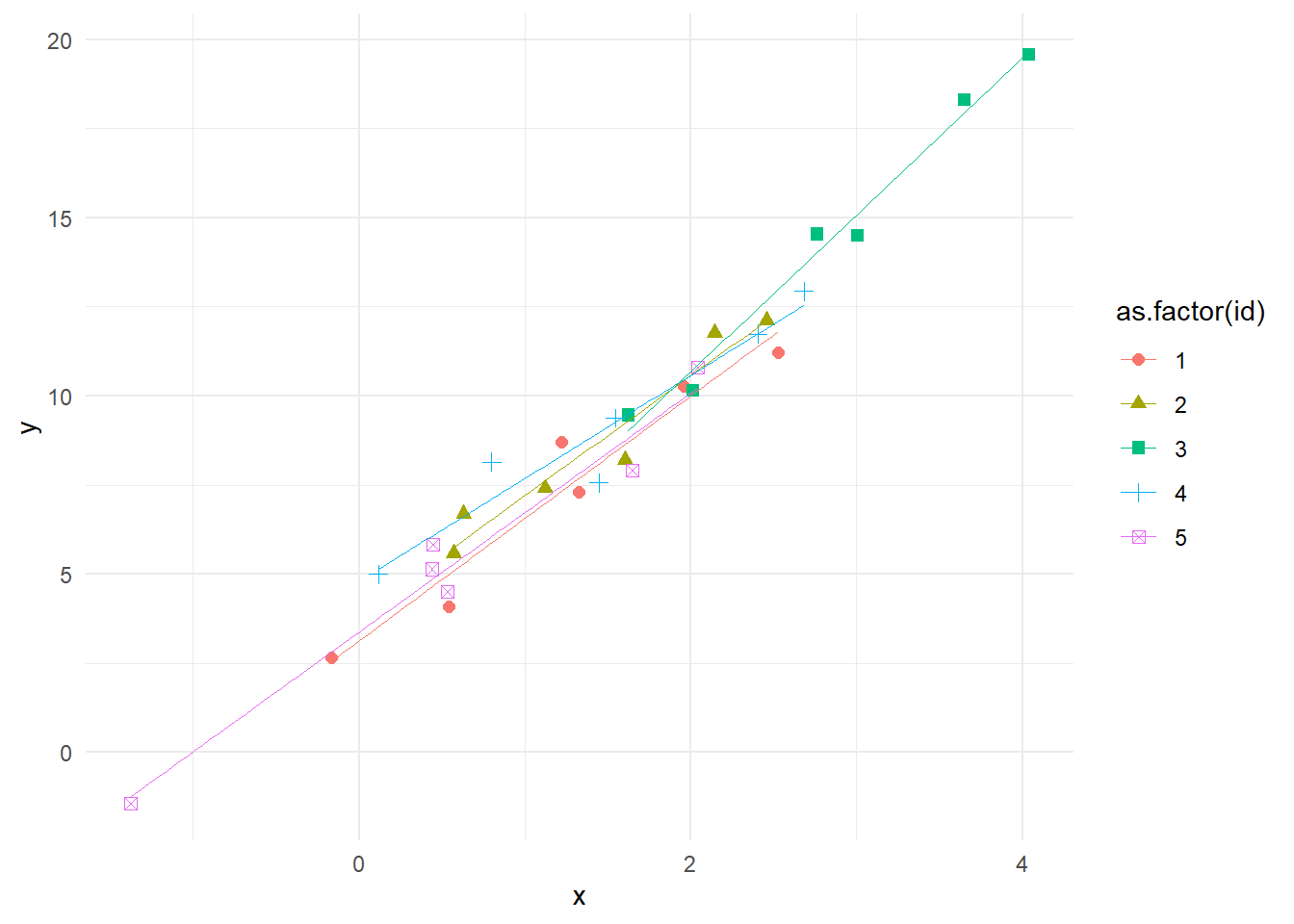

ggplot(data = df, mapping = aes(x = x, y = y, color = as.factor(id), shape = as.factor(id))) +

geom_point(size = 2) +

geom_smooth(method = "lm", se = F, linewidth = 0.1) +

theme_minimal()Rows: 30

Columns: 6

$ id <int> 1, 1, 1, 1, 1, 1, 2, 2, 2, 2, 2, 2, 3, 3, 3, 3, 3, 3, 4, 4, …

$ time <int> 1, 2, 3, 4, 5, 6, 1, 2, 3, 4, 5, 6, 1, 2, 3, 4, 5, 6, 1, 2, …

$ id_effect <dbl> 1.532956, 1.532956, 1.532956, 1.532956, 1.532956, 1.532956, …

$ x <dbl> 1.2236166, 0.5428839, -0.1687838, 1.9596749, 1.3257576, 2.52…

$ epsilon <dbl> 0.88224874, -1.35440156, -0.28777985, -0.12369397, -0.866977…

$ y <dbl> 8.697863, 4.078648, 2.654433, 10.268124, 7.306130, 11.229566…

説明変数 x 固定効果 id_effect の相関を確認します。

cor(df$x, df$id_effect)[1] 0.6214152固定効果を考慮せずに線形回帰モデルを確認します。

lm(data = df, formula = y ~ x) %>% summary()

Call:

lm(formula = y ~ x, data = df)

Residuals:

Min 1Q Median 3Q Max

-1.5614 -0.6340 -0.0320 0.7304 1.8422

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.3356 0.2781 11.99 1.5e-12 ***

x 3.7154 0.1455 25.53 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9177 on 28 degrees of freedom

Multiple R-squared: 0.9588, Adjusted R-squared: 0.9573

F-statistic: 651.8 on 1 and 28 DF, p-value: < 2.2e-16固定効果を考慮した線形回帰モデルを確認します。

# 個体ごとの平均値を計算

df_means <- aggregate(. ~ id, data = df[, c("id", "y", "x")], FUN = mean)

names(df_means)[names(df_means) == "y"] <- "y_mean"

names(df_means)[names(df_means) == "x"] <- "x_mean"

df <- merge(df, df_means, by = "id")

# 各変数を平均値からの偏差に変換

df$y_demeaned <- df$y - df$y_mean

df$x_demeaned <- df$x - df$x_mean

# 偏差データを用いた線形回帰(最小二乗法)

X <- matrix(df$x_demeaned, ncol = 1)

Y <- matrix(df$y_demeaned, ncol = 1)

# 説明変数xの係数

beta_hat <- solve(t(X) %*% X) %*% t(X) %*% Y

# 残差の計算

residuals <- (Y - X %*% beta_hat) %>% as.vector()

# 残差平方和の計算

RSS <- sum(residuals^2)

# 自由度 (n - k)

k <- ncol(X)

n <- nrow(X)

degrees_of_freedom <- n - k - n_id

# 誤差分散の推定

sigma2_hat <- RSS / degrees_of_freedom

# 共分散行列の計算

var_beta_hat <- sigma2_hat * solve(t(X) %*% X)

# 標準誤差の計算

se_beta_hat <- sqrt(diag(var_beta_hat))

# 95%信頼区間の計算

alpha <- 0.05

critical_value <- qnorm(1 - alpha / 2) # 正規分布の臨界値

lower_ci <- beta_hat - critical_value * se_beta_hat # 下限

upper_ci <- beta_hat + critical_value * se_beta_hat # 上限

# 結果のまとめ

data.frame(beta_hat, var_beta_hat, se_beta_hat, lower_ci, upper_ci, check.names = F) beta_hat var_beta_hat se_beta_hat lower_ci upper_ci

1 3.468962 0.0321274 0.1792412 3.117656 3.820268関数 plm{plm} を利用して固定効果モデルを求めます。

library(plm)

pdata <- pdata.frame(df[, c("id", "time", "x", "y")], index = c("id", "time"))

fixed_model <- plm(y ~ x, data = pdata, model = "within")

summary(fixed_model)Oneway (individual) effect Within Model

Call:

plm(formula = y ~ x, data = pdata, model = "within")

Balanced Panel: n = 5, T = 6, N = 30

Residuals:

Min. 1st Qu. Median 3rd Qu. Max.

-1.374630 -0.595977 -0.023057 0.586923 1.444243

Coefficients:

Estimate Std. Error t-value Pr(>|t|)

x 3.46896 0.17924 19.354 3.77e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Total Sum of Squares: 304.44

Residual Sum of Squares: 18.332

R-Squared: 0.93978

Adj. R-Squared: 0.92724

F-statistic: 374.562 on 1 and 24 DF, p-value: 3.7698e-16分散共分散行列を確認します。

fixed_model$vcov x

x 0.032127495%信頼区間を確認します。

confint(fixed_model, level = .95) 2.5 % 97.5 %

x 3.117656 3.820268以上です。