Rの関数から VAR {vars} 引数 exogen の利用 を確認します。

本ポストはこちらの続きです。

Rの関数:VAR {vars} 引数 season の利用

Rの関数から VAR {vars} 引数 season の利用 を確認します。本ポストはこちらの続きです。シミュレーションの設計データの構造:四半期データ(1年=4期)を想定し、season = 4 を設定します。季節性の導入:変数A (S...

www.saecanet.com

2026.01.03

シミュレーションの設計

- データの構造:

- 内生変数 (

y_1,y_2): 互いに影響し合う2つの変数(VAR構造)。 - 外生変数 (

x): システムの外側からy_1,y_2に「衝撃(ショック)」を与える変数。yはxに影響を与えません。

- 内生変数 (

- 係数の設定:

- VAR係数 (内生): 以前と同様のラグ構造を設定します。

- 外生係数:

-

xがy_1に与える影響: +2.0 -

xがy_2に与える影響: -1.5

-

- 目的:

-

exogen引数を使ってモデルを推定した際に、VARのラグ係数だけでなく、「外部からの衝撃の効果(+2.0 と -1.5)」を正しく分離して推定できるかを確認します。

-

なお、有意水準は5%とします。

Rコード

外生変数 (exogen) を含むVARデータの生成

-

観測数: 200 -

内生変数: Endo_A, Endo_B (相互に影響) -

外生変数: Exogen_X (外部から Endo_A, Endo_B に影響を与える) -

真の外生係数: Endo_Aへの影響 = +2.0, Endo_Bへの影響 = -1.5

# パッケージの読み込み

library(vars)

library(ggplot2)

library(tidyr)

# 乱数シードの固定

seed <- 20260103

set.seed(seed)

# 設定: 2変量VAR(1) + 1変量外生変数

n_obs <- 200

# 1. VARの真の係数 (内生変数のラグ効果)

# y1(t) = 0.5 * y1(t-1) + 0.2 * y2(t-1) ...

# y2(t) = -0.3 * y1(t-1) + 0.4 * y2(t-1) ...

A_true <- matrix(c(0.5, 0.2, -0.3, 0.4), nrow = 2, byrow = TRUE)

# 2. 外生変数の係数 (Impact of Exogenous Variable)

# x(t) が現在の y1, y2 に与える影響

# y1 に対して: +2.0

# y2 に対して: -1.5

B_exogen <- matrix(c(2.0, -1.5), nrow = 2)

# 外生変数 x の生成 (ランダムな外部ショック)

# 正規乱数で生成

x_t <- rnorm(n_obs, mean = 0, sd = 1)

# データ生成

data_y <- matrix(0, nrow = n_obs, ncol = 2)

colnames(data_y) <- c("Endo_A", "Endo_B")

# 初期値

y_prev <- matrix(c(0, 0), ncol = 1)

for (t in 2:n_obs) {

# 外生変数の値 (現在の時点 t の値を使用)

x_curr <- x_t[t]

# y(t) = A * y(t-1) + B * x(t) + error

# ここで x(t) が加算される点が重要です

y_curr <- A_true %*% y_prev + B_exogen * x_curr + rnorm(2, sd = 0.5)

data_y[t, ] <- as.vector(y_curr)

y_prev <- y_curr

}

# データフレーム化

df_sim <- as.data.frame(data_y)

df_sim$Exogen_X <- x_t

df_sim$Time <- 1:n_obs

# データの可視化

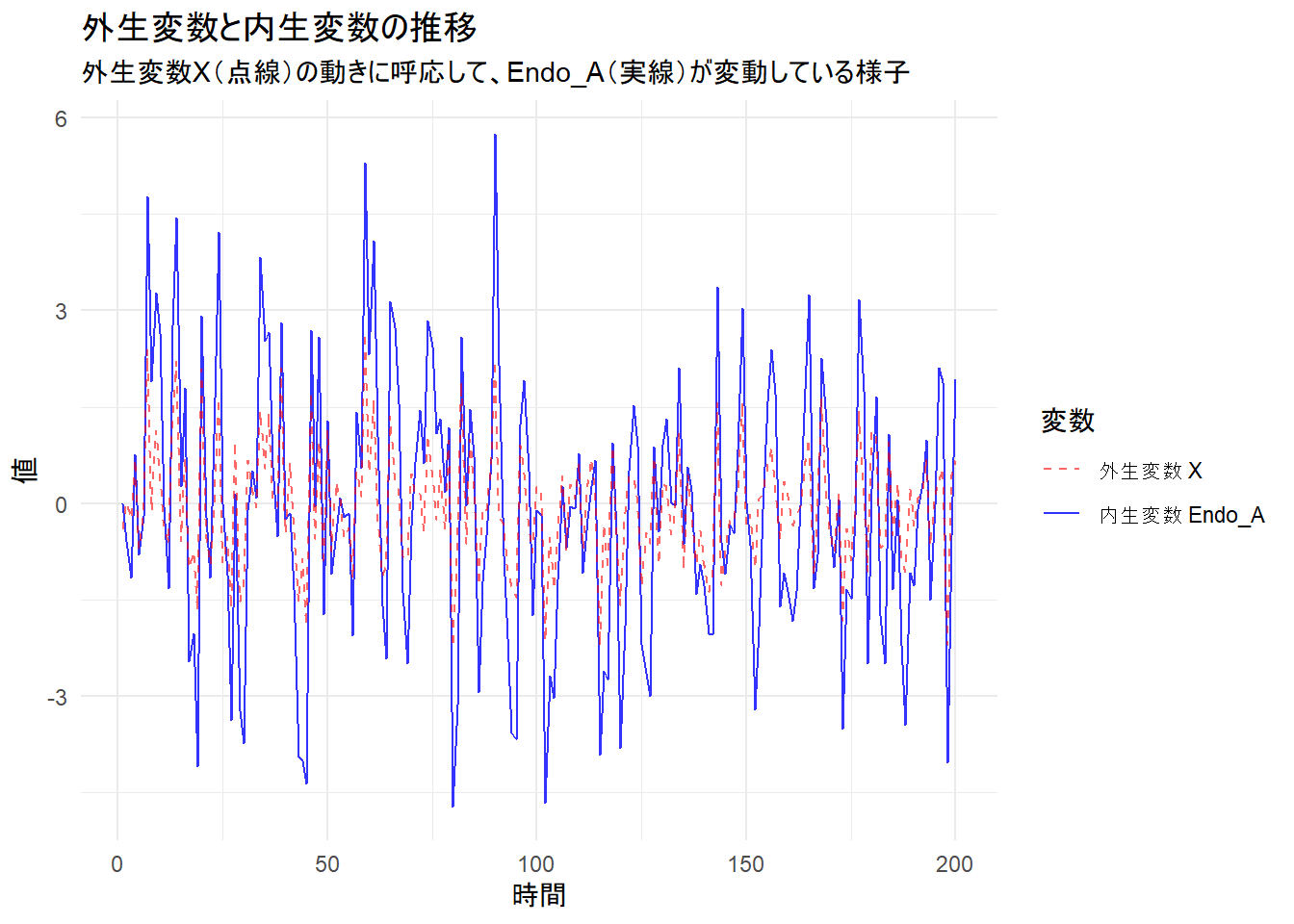

# 外生変数Xと、内生変数Endo_Aの動きを比較

p1 <- ggplot(df_sim, aes(x = Time)) +

geom_line(aes(y = Endo_A, color = "内生変数 Endo_A"), alpha = 0.8) +

geom_line(aes(y = Exogen_X, color = "外生変数 X"), alpha = 0.6, linetype = "dashed") +

labs(

title = "外生変数と内生変数の推移",

subtitle = "外生変数X(点線)の動きに呼応して、Endo_A(実線)が変動している様子",

x = "時間", y = "値"

) +

scale_color_manual(name = "変数", values = c("内生変数 Endo_A" = "blue", "外生変数 X" = "red")) +

theme_minimal()

print(p1)

VARモデルの推定 (exogen引数の利用)

# 推定の実行

# y引数には内生変数のみを渡す

# exogen引数に外生変数を渡す

# exogenの行数は y と同じである必要があります

exogen_data <- matrix(df_sim$Exogen_X, ncol = 1)

colnames(exogen_data) <- "Exo_X"

var_exogen <- VAR(

y = df_sim[, c("Endo_A", "Endo_B")],

p = 1,

type = "const",

exogen = exogen_data

)

print(summary(var_exogen))

VAR Estimation Results:

=========================

Endogenous variables: Endo_A, Endo_B

Deterministic variables: const

Sample size: 199

Log Likelihood: -279.56

Roots of the characteristic polynomial:

0.5578 0.5578

Call:

VAR(y = df_sim[, c("Endo_A", "Endo_B")], p = 1, type = "const",

exogen = exogen_data)

Estimation results for equation Endo_A:

=======================================

Endo_A = Endo_A.l1 + Endo_B.l1 + const + Exo_X

Estimate Std. Error t value Pr(>|t|)

Endo_A.l1 0.547005 0.028013 19.527 < 2e-16 ***

Endo_B.l1 0.262998 0.029923 8.789 7.83e-16 ***

const -0.002462 0.035989 -0.068 0.946

Exo_X 1.958758 0.038473 50.913 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5027 on 195 degrees of freedom

Multiple R-Squared: 0.9419, Adjusted R-squared: 0.941

F-statistic: 1053 on 3 and 195 DF, p-value: < 2.2e-16

Estimation results for equation Endo_B:

=======================================

Endo_B = Endo_A.l1 + Endo_B.l1 + const + Exo_X

Estimate Std. Error t value Pr(>|t|)

Endo_A.l1 -0.31016 0.02699 -11.494 <2e-16 ***

Endo_B.l1 0.41958 0.02883 14.556 <2e-16 ***

const 0.01328 0.03467 0.383 0.702

Exo_X -1.49642 0.03706 -40.377 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4843 on 195 degrees of freedom

Multiple R-Squared: 0.9388, Adjusted R-squared: 0.9378

F-statistic: 996.6 on 3 and 195 DF, p-value: < 2.2e-16

Covariance matrix of residuals:

Endo_A Endo_B

Endo_A 0.2527439 0.0001642

Endo_B 0.0001642 0.2345434

Correlation matrix of residuals:

Endo_A Endo_B

Endo_A 1.0000000 0.0006746

Endo_B 0.0006746 1.0000000Endo_A の方程式:外部からのプラスの衝撃

シミュレーション設定(真の値):

- ラグ効果:

- 自身の過去(

0.5)、相手の過去(0.2)

- 自身の過去(

- 外生効果:

- 外部ショックXから +2.0 の影響

結果の解釈

-

Endo_A.l1(0.547) &Endo_B.l1(0.263):- 真の値 (

0.5と0.2) に近い値が推定されています。自己回帰の構造が正しく捉えられています。

- 真の値 (

-

Exo_X(1.959):- 真の値 2.0 に近い値が推定され、p値は設定した有意水準を下回っています。 「外部要因Xが1単位増えると、Endo_Aは2単位増える」という関係性を特定できています。

Endo_B の方程式:外部からのマイナスの衝撃

シミュレーション設定(真の値):

- ラグ効果:

- 相手の過去(

-0.3)、自身の過去(0.4)

- 相手の過去(

- 外生効果:

- 外部ショックXから -1.5 の影響

結果の解釈

-

Endo_A.l1(-0.310) &Endo_B.l1(0.420):- こちらも真の値 (

-0.3と0.4) に近い値となっています。

- こちらも真の値 (

-

Exo_X(-1.496):- 真の値 -1.5 とほぼ一致しており、p値は設定した有意水準を下回っています。 「外部要因Xが増えると、Endo_Bは減少する」という逆方向の因果関係も特定できています。

モデル全体の評価

- 決定係数 (Multiple R-Squared):

- 両方程式ともに 約0.94 と高い値を示しています。これは、内生変数の変動のほとんどが、「過去の履歴」と「現在の外部ショック」によって説明できていることを意味します。

- 残差の相関 (Correlation matrix of residuals):

- Endo_A と Endo_B の残差間の相関は 0.00067 とほぼゼロです。モデルが構造(ラグと外生要因)を適切に吸い上げたため、残った誤差には何の関係性も残っていない状態です。

以上です。